Domestic equities have served SMSF investors well in recent times, but as Ashley Pittard reports, all factors are pointing towards a greater allocation to overseas markets.

In the past 15 years, there have been dramatic changes within global and Australian markets, and further evolution is occurring.

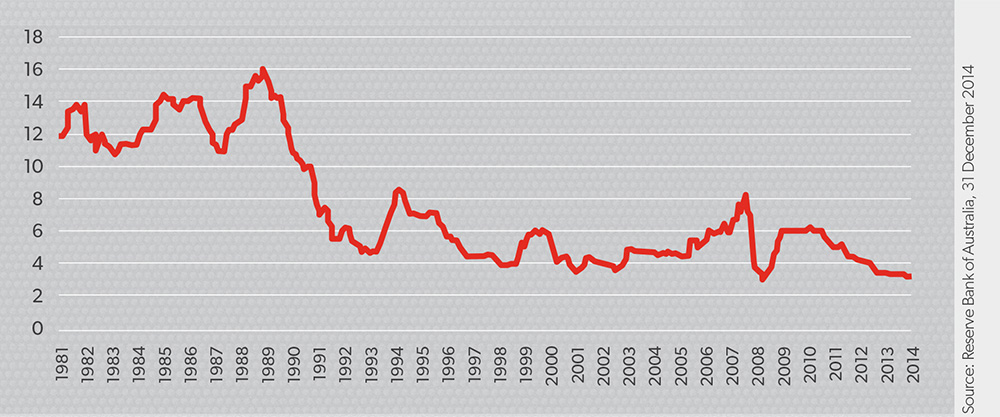

Interest rates

In 1989, term deposit rates ranged up to 17 per cent. The industry was essentially a cashbook. We sit here today with interest rates at all-time lows. The industry has been forced to adapt in this extended lower interest rate environment and look for different asset classes to provide returns.

Technology

Australia has been directly affected by the universal revolution in technology, most notably with the advent of the information superhighway, the World Wide Web, which provided the foundation for another explosion, namely social media. Surplus information is at our fingertips, thus the ability to decipher value from noise has dramatically increased and sticking to investment processes is increasingly important.

Demographics

Demographics in Australia are changing: most notably we are ageing. This has affected the demand for certain financial products and, looking into the future, it may dull Australia’s economic growth and put greater strain on the government and its policies.

Commodity boom

Australia has been fortunate enough to benefit from one of the largest commodity booms in history spanning well over a decade. As this boom has ended, Australians are slowly realising the need for the economy to diversify away from the mining and commodities sectors in order to survive and prosper.

Figure 1: One-year retail term deposit rates (%)

Global financial crisis

Australia was by no means impervious to the global financial crisis (GFC), however, on a relative basis to elsewhere in the world, it maintained a strong financial system due to the stricter and more robust regulatory structure in place and timely fiscal stimulus. This has had numerous implications, including large capital flows into the country and a persistently high Australian dollar due to our relatively attractive interest rates.

Globalisation of markets

Markets are becoming less segmented and more integrated. Industry factors are becoming more important than country factors in determining a company’s risk and return. This means taking a regional view on investing makes increasingly little sense.

There has been a plethora of other changes over the past few decades: the choice of super fund regime was implemented, products like exchange-traded funds have materialised, and bond yields have widened and tightened.

Meanwhile, back at the investment managers’ ranch, trust has come and gone and conservatism is again the new normal.

2013 was an inflection point

In 2013, relativities in interest rates, currency and the share market in Australia compared to the rest of the world started to change. This was combined with government bond yields starting to rise around the world.

In the previous 10 and 20 years in Australia, deteriorating bond yields and convincing economic growth driven by the commodities boom led to very strong investment results.

Looking forward, however, the view is somewhat different.

The Australian share market started to underperform international equities in 2013 as the resources boom moved into a transition stage, and faster growth in the United States and slower growth in China prevailed.

The economy’s real gross domestic product growth rate is entering 2015 below trend, consumer confidence is down, income growth outlook is bleak and the residential property market has become overheated.

In the past six months, Australia’s stock market has been in a mundane, corrective phase and is out of sync with world markets. Although certain stocks and sectors have retracted 20 per cent to 30 per cent and may be back to more normalised levels, we struggle to see where these businesses will find earnings growth in the medium term and believe the outlook is tough.

What has the chase for yield cost us?

The extended low interest rate environment has made us chase returns from non-cash assets. Inopportunely, investors often chase what has recently performed well, yet recent returns present trivial future guidance and history shows chasing what has performed well rather than what will perform well often ends poorly.

The overarching theme propelling many investment decisions has been this chase for yield triggered by the franking credit system.

Yet the majority of Australian stocks have priced in the value of franking credits and investors are overstating their worth, especially compared to the long-term advantage of owning a growing and profitable company.

Australians need to focus on total return. Owning a portfolio of high-yielding companies with ordinary prospects may deliver suboptimal results and in this environment may expose investors to significant capital losses.

Owning a share in a quality business, which can be expected to grow earning and thus their payments to shareholders, is a far better total return strategy.

Other challenges

Currency

The Australian dollar has fallen 13 per cent over the past six months against the US dollar, as at 31 December 2014, yet at US$0.81 it is substantially higher than its historical average since floating of US$0.77.

We still think there is further to go, likely towards the 70c mark, as interest rate differentials between the US and Australia close and the full impact of the decline in commodity prices washes through.

Exposing your investment portfolio to overseas currencies, which have the capacity to appreciate relative to the Australian dollar, can enhance returns and aid diversification benefits.

Where does the opportunity exist?

Limited opportunity onshore

The Australian share market has become very concentrated and is dominated by two industries, financials and resources, which are highly correlated, and thus over 60 per cent of the Australian index can be almost replicated in two stocks.

Australia’s big banks have soared to become some of the most expensive in the world by nearly every measure and the International Monetary Fund recently released research indicating Australia may have the world’s second-most expensive housing market behind Belgium.

When we turn our attention to resources, we continue to see downside risk due to China’s slowing economic growth. Despite the dramatic correction over the previous six months, we think prices are still above trend valuation, according to the cost curve, and have further to fall.

This means the two largest industries in Australia, occupying over 60 per cent of the index, provide futile ground for new investment.

When we look to the world index, not only do we see more value in these sectors, but also we are able to gain exposure to industry sectors not well represented here in Australia.

For example, try finding a Google or Apple in Australia; in fact, information technology as a sector represents a mere 1 per cent of the ASX 200 Index.

Lack of portfolio diversification is concerning

It has long been recognised asset allocation, not security selection, is the key driver of long-term investment results.

One of the most powerful insights of modern portfolio theory is the finding that allocating capital across risky assets can actually reduce overall portfolio risk, due to the benefits of diversification.

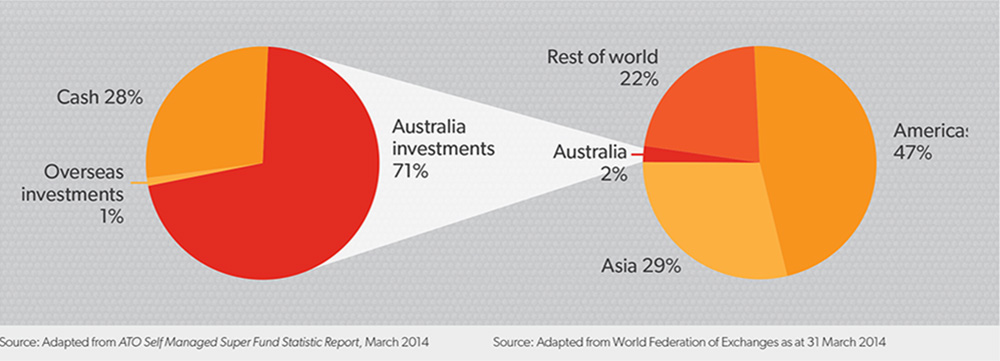

Basic behavioural finance warns us of home market bias and yet familiarity has prevailed and SMSF portfolios are inherently overweight in Australian investments.

The domestic share market represents less than 2 per cent of the world’s companies, however, SMSFs have more than 71 per cent of their assets in Australian investments and only 1 per cent in overseas investments.

This makes little sense and adds unnecessary concentration risk, especially when we combine that with the fact the assets we hold the most of are expensive and have lacklustre growth prospects.

Combined with the elevated currency, it would suggest that now is a good time to start moving assets offshore.

Figure 2: SMSF asset allocations and % of global market capitalisation

Better select risk/reward opportunities globally

It has long been recognised asset allocation, not security selection, is the key driver of long-term investment results. One of the most powerful insights of modern portfolio theory is the finding that allocating capital across risky assets can actually reduce overall portfolio risk, due to the benefits of diversification.

Not only are there more opportunities offshore, but in many cases they present a more compelling investment case. Our favoured industries include:

Property

We look for areas of the property market, which has had severe declines in asset values, such as the US and Europe post the GFC. This opportunity was created by a growing supply and demand imbalance; new construction was virtually non-existent as developers became either bankrupt or severely constrained by the banks. As rents were at lows and yields at highs, it caused depressed asset prices, down by between 40 per cent and 70 per cent from their peak. It is very important to be selective in different geographical markets as they are affected by their respective economy. Ireland and Spain are the two markets we are most attracted to within Europe as we see a strong prospect of solid earnings growth, which will drive further valuation expansion.

Banks

We favour select offshore banks as they stand to gain from upticks in interest rates and expected loan growth as the housing market recovers. The banks we favour are those that can capitalise on this through their domestic focus and commitment to paying profits out to shareholders in the form of dividends, just as the Australian banks did after the property crisis in the 1990s, which has resulted in them becoming some of the most profitable and expensive in the world, and their shareholders handsomely rewarded. Wells Fargo in the US and Lloyds in the United Kingdom are two prime examples.

Service providers

We are attracted to dominant service providers with an entrenched market leadership position. Exchanges are an exemplary illustration of this. They are attractive, scale businesses that have low capital expenditure requirements and provide a high return on equity. We favour futures exchanges over equity exchanges due to their monopolistic characteristics and pricing power, and should stand to gain when interest rates in the US increase. We favour the Intercontinental Exchange and Chicago Mercantile Exchange.

Asia

When we look to investments in Asia, old world China is not our focus as hard asset investment is slowing and the banking sector remains over-extended. We are finding genuine value in industries supported by rising domestic consumption or that are benefiting from changes to consumer consumption patterns. These structural growth stories coupled with sound business fundamentals, which are not largely affected by the macroeconomic environment, are our main target. We are focused on gaming, internet and consumer names.

Will passive strategies achieve the results we require?

The market has become increasingly fixated on low fees and thus index-hugging approaches have prevailed in popularity. Yet regardless of the market environment, holding an index means holding a bit of everything.

Our investment philosophy is about knowing what you own and only owning the top names you favour. It sounds basic, yet index investing contradicts this very notion.

Passive strategies have their place in the market, and in fact provide stock-pickers such as ourselves with the opportunity to buy the companies we like at attractive prices.

However, if your strategy is to maximise your Australia-domiciled, after-tax investment returns over the longer term, we believe fundamental stock-picking is the way to achieve this.