Grant Abbott outlines why 2014 has all the makings of a prosperous year for SMSF practitioners.

Is 2014 going to be your best ever SMSF year? If it is, then read on and get moving because there is no time to waste. If you haven’t decided yet, then still read on and I’ll guarantee you’ll have your answer in 10 minutes.

First off there are two simple questions that will set this year apart as an amazing SMSF year for you professionally and personally.

1. Do you intend 2014 to be different for you than 2013?

2. Is SMSF growth in the top three of your most important things in 2014?

If you expect 2014 is going to be the same as 2013, then forget about your best SMSF year ever as you are only going to repeat last year’s mistakes and last year’s wins will be just that, last year’s.

It is time to start afresh, take what worked last year and apply it in the context of the new strategies and technology that are in play. Look at the administration space for instance. Who ever thought AMP would buy the lion’s share of the major SMSF administration platforms to build their SMSF trustee distribution at a rapid pace?

For 2014, change, adapt and implement needs to be your mantra. Let’s face it, if you don’t change while everything changes around you, then you’ll get left behind and if you are running a business, that means harder and harder days are ahead. In a $550 billion industry, that is not right.

I have witnessed the SMSF industry changing this way and that since SMSFs were first introduced 20 years ago in 1994. Some accounting firms, advisers and financial planners adapt, grow and prosper and others give up. I remember speaking at a professional development session in May 1998, a week after the budget, where the government smashed related trusts, which were all the rage for borrowing purposes, and got rid of the regulator, the Insurance and Superannuation Commission, putting the Australian Taxation Office (ATO) in its place.

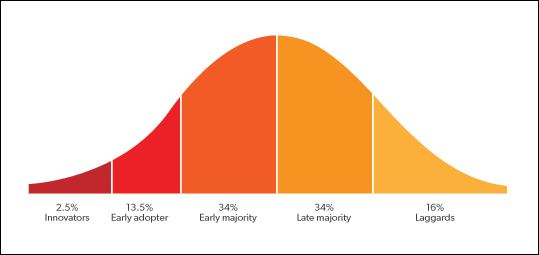

Diagram 1: The curve

At that time, accountants practising in the SMSF space were surveyed on their business intentions and a sizeable percentage surprisingly decided to get out of SMSFs and leave superannuation to financial planners. The prospect of change turned many of these early 1990s adopters of SMSFs into fearful laggards who have no doubt come back into the SMSF game over the past few years chasing the big fish. What could have been? I learnt from one of my mentors to “always look for an opportunity in a change or crisis” and it has proved my most profitable belief.

On the second question of things important to you, it is an established psychological fact that individuals spend most of their time on the top three things that are currently important to them in their life. If it is not top three, then it will not be achieved – so reshape your top priorities to include SMSFs.

Let’s take some time now to consider six of the most important emerging SMSF business, strategy and advising trends for 2014.

1. SMSF-friendly government

For the past seven years, SMSFs have not been on the government’s agenda and that has allowed so many of the other industry players to take pot shots at the sector, particularly around SMSF lending. With the new coalition government, we have a team committed to getting rid of the red tape and guaranteeing there will be no major changes to super in its first term (governments change, not cases or ATO rulings and guidelines). In addition, Assistant Treasurer Arthur Sinodinos is very supportive of SMSFs and is of the view they are leading the change in superannuation, causing their big brothers – the industry and retail super funds – to make ‘SMSF-like’ member products. Given the longevity of past governments, it should be safe to assume the coalition will be looking after the SMSF space until late 2019.

2. Murray review of financial services

The Murray review will be big and expect many changes to SMSFs in the medium term. The last financial services review was the Wallis inquiry in 1997 and that resulted in some major changes to SMSFs, with the ATO installed as the new regulator based on its recommendations. At that time, SMSFs were a very minor player in financial services, with only $40 billion in assets. With SMSF assets to hit $1 trillion by 2020, expect some major moves impacting on all of us in the superannuation industry. It is too big to fail, but not too big to be changed or plundered

3. The curve

This is my favourite big picture analytical tool and comes from marketing analysis. In short, with any new service, product, strategy or business there is a take up and an adoption cycle the product, service, strategy or business must go through.

As can be seen in Diagram 1, the curve always starts with the innovators, who get in early, build and develop the market, for example, Google, Facebook, Toyota Hybrid and LinkedIn. The next in line and the one the innovators want to help drive the product brand is the early adopters. The early adopters are the ones that try the product, strategy or service, test it and, if it works, move quickly to implement, execute and profit. We all know them and they are the first ones with the new gadget, the latest website or app or best strategy.

The early majority are more sanguine, preferring to let the early adopters take the lead, but at some stage the early majority moves and moves quickly to adoption. Of course, the big profits the early adopters and innovators have extracted are not on offer, but there is still good money to be had.

Eventually the service or product becomes standard and for many they cannot stay with their current offering no matter how hard it may be to learn about and use a new product, service or strategy. This is the realm of the late majority. But despite all efforts, there are some who will never move and it is more likely the product or service will become obsolete before this group moves. With current social media and the Internet, product cycles can move very quickly. Just look at the take up of Facebook.

So how does the curve play out for the war generation and SMSFs? As noted earlier, we are in the laggards when it comes to the war generation as only a few who are working and under 75 could start an SMSF, given contribution restrictions. But consider it differently. For those war generation members already in SMSFs, and that is more than 100,000 of them, the strategy of warehousing an aged-care unit in the fund for withdrawal when needed is an SMSF strategy at the innovation level and starting to be populated by the early adopters.

4. The next big SMSF wave

SMSFs have largely had their day when it comes to the war generation and baby boomers as they will only attract the very late majority of boomers who have been sitting on the sidelines watching the growth of SMSFs. However, the big play is generation X, those Australians between the ages of 32 and 50, who have between them over $580 billion sitting in superannuation accumulation accounts in industry, retail and, for the early adopters of this generation, in an SMSF.

As this cohort moves toward retirement and engagement with super becomes a necessity, or their motivation comes from sources such as share trading or property acquisition in an SMSF, expect the numbers and the assets in SMSFs to grow. It is the next big wave any SMSF business owner needs to ride and build systems and processes for to make the most of this special and super affluent group.

5. Focus on innovation and early-adoption SMSF strategies

Advising a client on the establishment of a transition-to-retirement income stream is not challenging or profitable by itself because it is well known to the advising community and thus in the late majority, meaning it is inexpensive and ubiquitous. In fact, a number of SMSF trustees do it themselves. The strategies best to focus on, build tools for and find clients for are those at the early-adoption phase or if you are an SMSF innovator, then at the innovation stage. A few innovative SMSF strategies we are helping advisers make the most of are:

baby boomers and comprehensive estate planning inside and outside of superannuation,

generation X acquiring a property in an SMSF with a limited recourse borrowing arrangement (LRBA),

farmers transferring farms into a family SMSF for the end benefit of the child working on the farm,

incapacity planning and SMSF living wills with the war generation, and

excess concessional contribution strategies and contribution reserves.

6. Advising: strategy layering

Strategy layering is an emergent trend that is starting to take shape at the top end of the SMSF advising pool. Suffice to say the days of focusing on a single strategy, such as an LRBA or account-based pension, are now in the laggard days. Strategy layering consists of taking a single strategy, then placing another strategy on top of it to make the most of the initial strategy, like making one plus one equal three.

The classic layering strategy is for small business and looks like this:

- Establish SMSF.

- Transfer business real property into SMSF.

- Lease property back to business and receive rent.

Now, if it has been structured properly, then the client hopefully is in the pension phase so income flowing into the fund is tax free, while the entity, such as the family trust, is paying deductible rent. Another layer on top of this could be that the proceeds from the transfer of the property by the members, if not made as a contribution, could be used to pay down an outstanding division 7A loan. And with a little imagination there can be a number of layers of strategy on top of that.

With SMSFs only part of the total wealth creation structures for a client, layering strategies in the right order both inside and outside the fund is the highest level of strategic advice that can be aspired to in 2014.

Good luck.