The changes to the superannuation system passed as law in November included a drop in the Division 293 income threshold. Chris Boag notes the strategic use of self-funding instalment warrants could offer some relief for SMSF members affected by this amendment.

On 3 May last year, the federal government handed down its budget, which included changes to the superannuation system. Some of the proposed changes were quite controversial, particularly the $500,000 lifetime cap on non-concessional superannuation contributions that was backdated to 1 July 2007. Other measures introduced, such as the low-income superannuation tax offset and concessional catch-up contributions, were more favourable.

On 15 September, Treasurer Scott Morrison and Assistant Treasurer Kelly O’Dwyer announced changes to the proposals made on 3 May. Some of the proposed legislation included:

- the non-concessional contribution cap to be reduced to $100,000 a year from $180,000,

- he concessional contributions cap to be reduced to $25,000 a year from $30,000 for individuals aged 48 and younger, and $35,000 for individuals aged 49 and above, as well as introducing the ability to use unused concessional contributions from the past five years,

- a balance transfer cap of $1.6 million (the maximum amount you can transfer to a pension account),

- the ‘work test’ for those over the age of 65 was to be abolished, but is now to remain in place, and

- the Division 293 tax threshold of the Income Tax Assessment Act 1997 to be reduced from $300,000 to $250,000 (an additional tax on your superannuation contributions).

On 23 November, the Turnbull government announced it had secured parliamentary passage for the most comprehensive suite of superannuation reforms in a decade.

So the game has changed and the goalposts have been moved yet again.

The issue this article will address is the reduced threshold for Division 293 tax to $250,000 adjusted taxable income (ATI) from $300,000. However, the strategy is also relevant to the reduction in the concessional contribution cap to $25,000 a year.

The strategy involves the use of self-funding instalment warrants (SFI), which allow, individuals to:

- increase tax deductions,

- increase franking credits,

- provide leverage,

- increase portfolio diversification, and

- reduce tax payable.

What is an SFI?

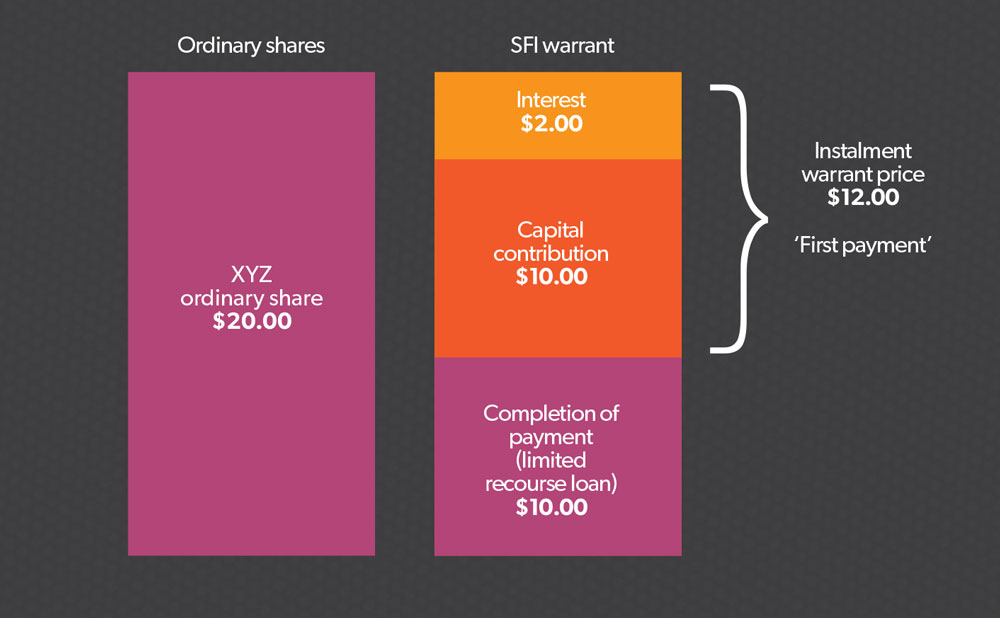

An SFI allows you to receive many of the benefits of owning Australian Securities Exchange (ASX)-listed securities without paying the full amount upfront. Instead, the SFI, as the name implies, allows you to acquire the ordinary share or exchange-traded fund (ETF) in two payments known as instalments. In fact, after paying the first instalment you receive many of the benefits of owning the ordinary share, such as potential capital growth, dividends and franking credits (if available), all for a lower upfront capital outlay. In effect you are using a limited recourse borrowing arrangement to leverage your share portfolio. You can either buy fewer shares to provide the desired ordinary share exposure or use the leverage to increase your exposure (Figure 1).

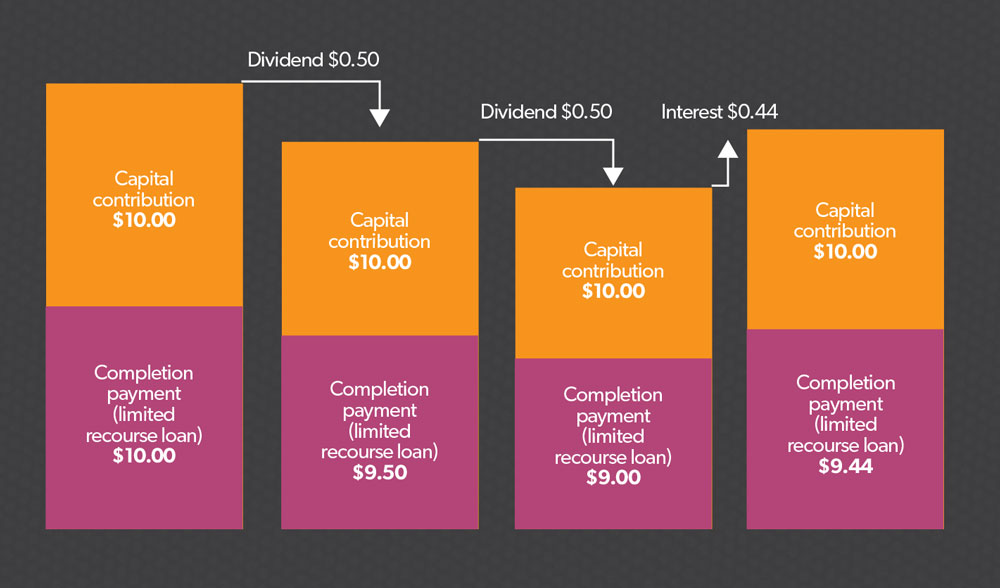

The dividends and interest are not directly payable to or by the investor, instead the dividend is used to offset the completion payment and any accrued interest (Figure 2).

Figure 1: How they work

Assumes SFI is purchased via an application, not on market.

Figure 2

Assumes ordinary share price of $20, interest at 4.4 per cent pa and dividens of 50c each declared and paid on the ordinary share.

Taxation

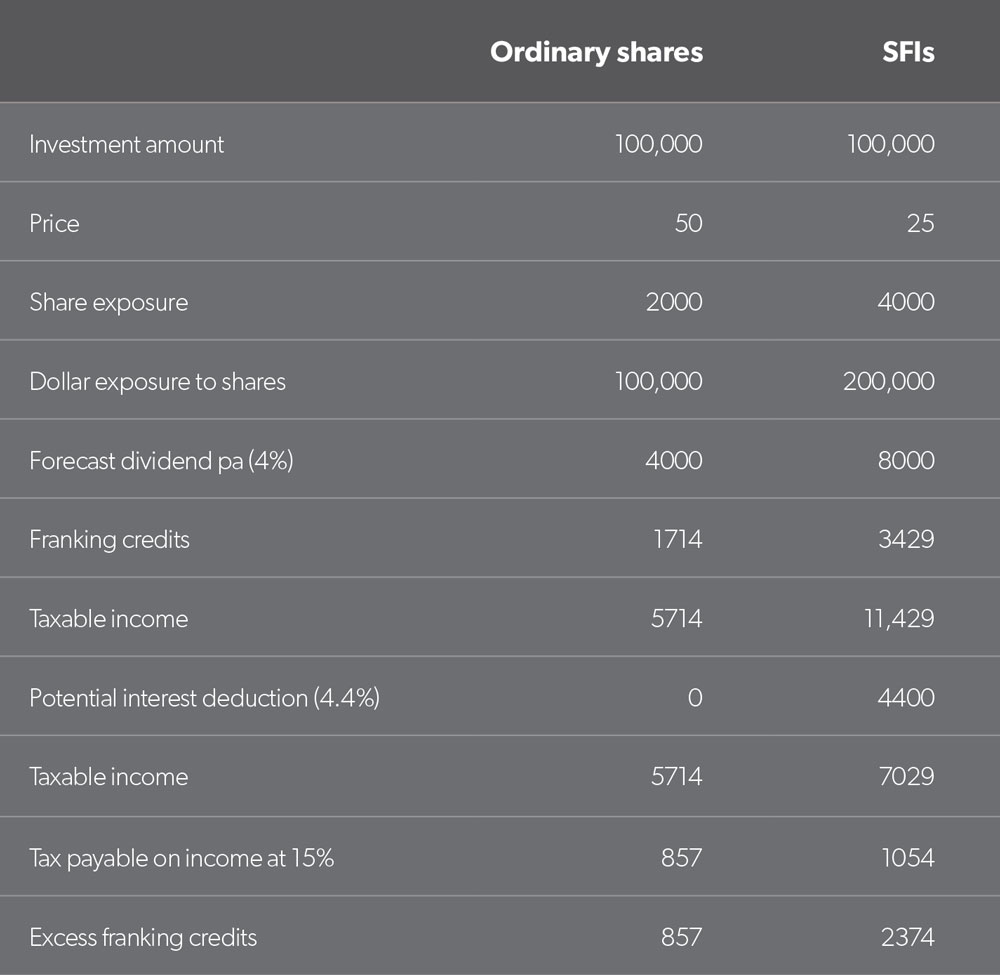

Using SFIs can help manage tax in an SMSF more effectively (Table 1). This is important for high-income earners now the Division 293 tax threshold will be reduced to $250,000 from $300,000 from 1 July 2017, meaning more investors will be caught by the tax. The SFI strategy helps by generating excess franking credits and a tax deduction within the portfolio. These franking credits are used to offset your tax payable, and remember, franking credits are fully rebatable so you can never have too much of a good thing. The interest on the loan is used as a deduction against the portfolio’s investment income, thus reducing the amount of income within the portfolio you are paying tax on.Another way of looking at it is that the gearing leverages your contribution. If you are restricted to a $25,000 concessional contribution, you can buy an SFI and gain, say, $50,000 of stock market exposure.

Table 1

Dividend is assumed to be 4 per cent a year and fully franked.

Interest rate is assumed to be 4.4 per cent and to be fully tax deductible. Assumes 50 per cent leverage for the SFI.

Portfolio construction

While the excess franking credit and interest deductions are attractive, it is important to remember that at this point the portfolio is geared. This can be great if the stocks you have invested in are going up in value. But this means that if the ordinary share rises or falls, the value of the SFI will rise and fall by a greater amount depending on the level of leverage. It is important to ensure you construct a portfolio that is well balanced and meets your documented SMSF investment strategy. Not all shares you may want to invest in will have a corresponding SFI, but that doesn’t mean you shouldn’t invest in them. If you construct the portfolio based on available SFIs only, you are likely to be scarifying portfolio balance for tax advantage and this has never been a wise choice. You must fundamentally want to invest in the ordinary share.

At Royston Capital we approach the portfolio construction by first determining the portfolio of ordinary shares that we wish to invest in. Where there is a suitable SFI we will replace the ordinary share with the SFI, but we don’t do this on a dollar-for-dollar basis. We tend to look at our level of exposure once gearing is taken into account. This helps to ensure we are not inadvertently increasing our exposure to a particular stock or sector and throwing out our desired portfolio objectives. The excess capital is then used to further increase the overall exposure to shares or to enhance the portfolio diversification by adding another asset class, such as international shares. This works particularly well for smaller portfolios that don’t have enough capital for a more diversified portfolio. The end result is a lower level of gearing, circa 30 per cent at the moment, but the impact is still there and importantly the portfolio is well balanced and performing in line with expectations plus gearing.

There is no doubt a portfolio constructed in this way can benefit SMSF investors. It will not suit everyone though. In order to invest in such a portfolio, you will need to have a long investment time frame, be willing to take on more risk and volatility with your portfolio, and be seeking to reduce contributions tax.