Infrastructure investments can cover a wide range of assets. Matt Bushby explains why it is important for investors to define the asset class more narrowly and looks at where some of the global opportunities now lie.

Infrastructure is the asset class made up of physical assets that provide essential services to society. Put simply, these are the services we use and interact with every single day. For instance, we use gas, water and electricity to carry out our daily activities and we also use infrastructure, such as rail and roads, to get from location to location.

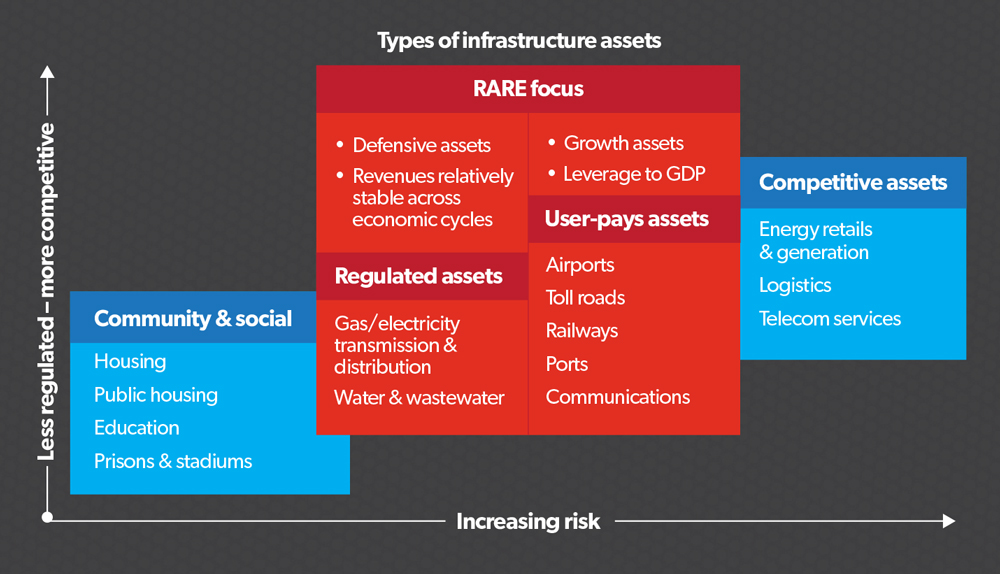

Broadly, infrastructure can be categorised into two key buckets: regulated assets and user-pays assets.

With regulated assets, the regulator determines the revenues a company should earn on their assets. If an asset earns too much, then the company is required to return some of its revenues to its customers by lowering prices. Conversely, if the asset earns too little, then the company is able to increase its prices. This mechanism leads to a relatively stable cash-flow profile over time. Additionally, the regulator periodically takes into account inflation, which means price increases are often linked to inflation. As such, these assets also act as a good hedge for inflation.

With user-pays assets, a company’s revenue is dependent on how many people use their assets. These physical assets, namely rail, airports, roads and telecommunications towers, move people, goods and services throughout an economy. Therefore as an economy grows, develops and prospers, these assets also typically grow. For instance, as more people use and to some degree depend on mobile phone data, we see mobile communications towers adding additional capacity to the physical towers to meet this demand.

Global focus

At Rare, we focus exclusively on global listed infrastructure. These are publically traded infrastructure securities such as the shares of electricity, water and airport companies. Listed infrastructure investors can enjoy the attractive characteristics of the infrastructure asset class, including long-term stable cash flows, lower correlation and beta to other asset classes and inflation protection, while enjoying the added benefits of listed markets such as liquidity and lower fees.Importantly, investing in listed markets provides us with the flexibility to take advantage of market movements and to invest where we, as active managers, see value.

One point we feel strongly on is what defines infrastructure. Upon our inception in 2006, we felt the existing infrastructure indices were flawed in numerous ways. Based on what we see as the key characteristics of infrastructure, we have created proprietary investment universes, bespoke to the requirements of each of our three active strategies. This framework has remained unchanged since our establishment and for more than 10 years.

Three pillars for investing

The way we think of infrastructure investing is simple – the companies we invest in must meet three key criteria. Firstly, the asset that the company owns must be a hard, physical asset. Secondly, this hard asset must provide an essential service to society or an economy. And lastly, there must be robust frameworks in place to ensure that we, the equity holders of the companies we invest in, get paid. This framework can be regulatory in nature or based on long-term concessional contracts. Both structures provide visibility over the company’s ability to generate cash flow.So when constructing our investable universe, the key characteristics we look for in a company come down to the stability of cash flows, as well as the level of predictability of these cash flows. In assessing this we will also look at the political and legal framework the company operates in and their pricing power.

Across our three investment universes, the companies held are either regulated utilities or owners of long-term concessional assets. By their very nature, these types of companies provide us with a high-level of confidence that they will have cash-flow generation well into the future.

Figure 1 summarises what types of infrastructure assets we focus on and which ones we exclude.

Figure 1: The infrastructure/risk continuum

Red flags

In constructing our investment universe, there are two main types of infrastructure assets we avoid. The first type is competitive assets that attract a higher risk relative to regulated and user-pays assets. Within the electricity sector, for instance, we are able to invest in the companies that own the electricity, transmission and distribution, however, we exclude from our investable universe the companies exposed to wholesale energy prices. These companies generate electricity and then sell it back to the electrical grid. As such they are subject to the forces of supply and demand, which in turn reduces the predictability and reliability of their cash flows. This lack of cash-flow predictability, among other things, increases their relative riskiness.

Airport services such as refuelling and baggage handling, for instance, are also excluded from our investable universe. This is because the companies that provide these services do not own the hard assets and have merely won a contract to provide these services. As there are no barriers to entry, such as regulation or long-term concessional agreements, there are limited safeguards in place to prevent another service provider from undercutting them on cost at contract renewal. This lack of framework increases the relative riskiness of these types of securities.

The second type is community and social assets, which include housing, public health, education and prisons. Firstly, these assets tend to be unlisted. As such there are limited opportunities in the listed market. While these assets are not competitive in nature, we exclude them from our investable universe as they often include property exposure and/or servicing and operating businesses. Generally their business models include availability-based payments, often inflation linked, for a defined contract term. During this period, contracts are unable to be repriced.

As a result, they have neither the protection of regulated assets in terms of the ability to reprice the contracts, say for changes in bond yields, or pass through of operating costs; nor the upside of infrastructure assets in terms of the benefit of volume improvements, namely exposure to economic growth. As a result, community and social assets tend to act as long-duration assets with significant real bond yield exposure.

Infrastructure opportunity and ‘Trump trade’

Infrastructure spending was a top issue in the recent United States presidential election and, as a result, the infrastructure opportunity is often referred to as the ‘Trump trade’. We don’t believe this is a fair assessment of the infrastructure opportunity. Since the US election there has been positive news and momentum; markets have rallied significantly on positive growth expectations and most recently on the December tax cuts. Within listed infrastructure, different sub-sectors have captured this upside to varying degrees. However, examining infrastructure as the ‘Trump trade’ is problematic on two accounts.Firstly, looking at infrastructure through the prism of a trade promotes short-termism, a costly behavioural bias that can see investors miss out on the long-term investment opportunities infrastructure can provide to their broader portfolio, namely diversification, inflation protection, stable cash flow and lower volatility.

Secondly, it focuses solely on the infrastructure needs of the US market. While there is no denying the US has substantial infrastructure needs, this country-specific view ignores the global opportunity. In developed markets, there is a strong need to refurbish existing, ageing infrastructure and to invest now to meet future needs. In emerging markets, as economies grow and individuals become wealthier, better quality infrastructure is needed. In these markets, we see increased demand for roads, airports and electricity assets. Also, with pressures on government budgets, we are seeing a gradual reduction in government ownership and their willingness to fund future infrastructure projects. This is leading to more opportunities for private capital in this asset class.

Trump’s increased focus on infrastructure has renewed investor interest in this asset class. However, what investors need to focus on are the benefits a diversified, global listed infrastructure allocation can provide to their broader portfolios.