The SMSF community asked the ATO for less frequent transfer balance account reporting requirements and was granted its request. However, Mark Ellem writes the framework allowing the lodgement of fewer pension event reports may make the administration of an SMSF even more complicated.

Commencing from 1 July, SMSFs will be required to report events to the ATO that impact on a member’s transfer balance account (TBA). This reporting is required to assist the ATO to track an individual’s TBA and to administer the tax consequences if the member’s transfer balance cap (TBC) is exceeded.

In terms of the frequency of reporting, the SMSF sector asked for special dispensation for SMSFs with smaller member balances and after months of deliberations, the ATO agreed. However, reliance on the ATO’s relaxed reporting rules is not without its risks and these risks should be understood by SMSF trustees and advice providers.

How will the relaxed reporting rules work?

Unlike other types of superannuation funds, which will generally be required to report relevant events on a monthly basis, an SMSF’s reporting time frames will be determined by the total superannuation balance (TSB) of its fund members. Where all members of the SMSF have a TSB of less than $1 million, the SMSF can report the relevant events at the same time as when its annual return is due. If the SMSF has any members with a TSB of $1 million or more, the relevant events must be reported within 28 days after the end of the quarter in which the event occurs.

Importantly, SMSFs are only required to assess their reporting frequency in relation to the $1 million threshold on 30 June immediately prior to the first income stream commencing in the fund. Once the fund’s reporting frequency has been determined, it will not change regardless of what happens to the member’s TSB thereafter or even if new pensions are commenced.

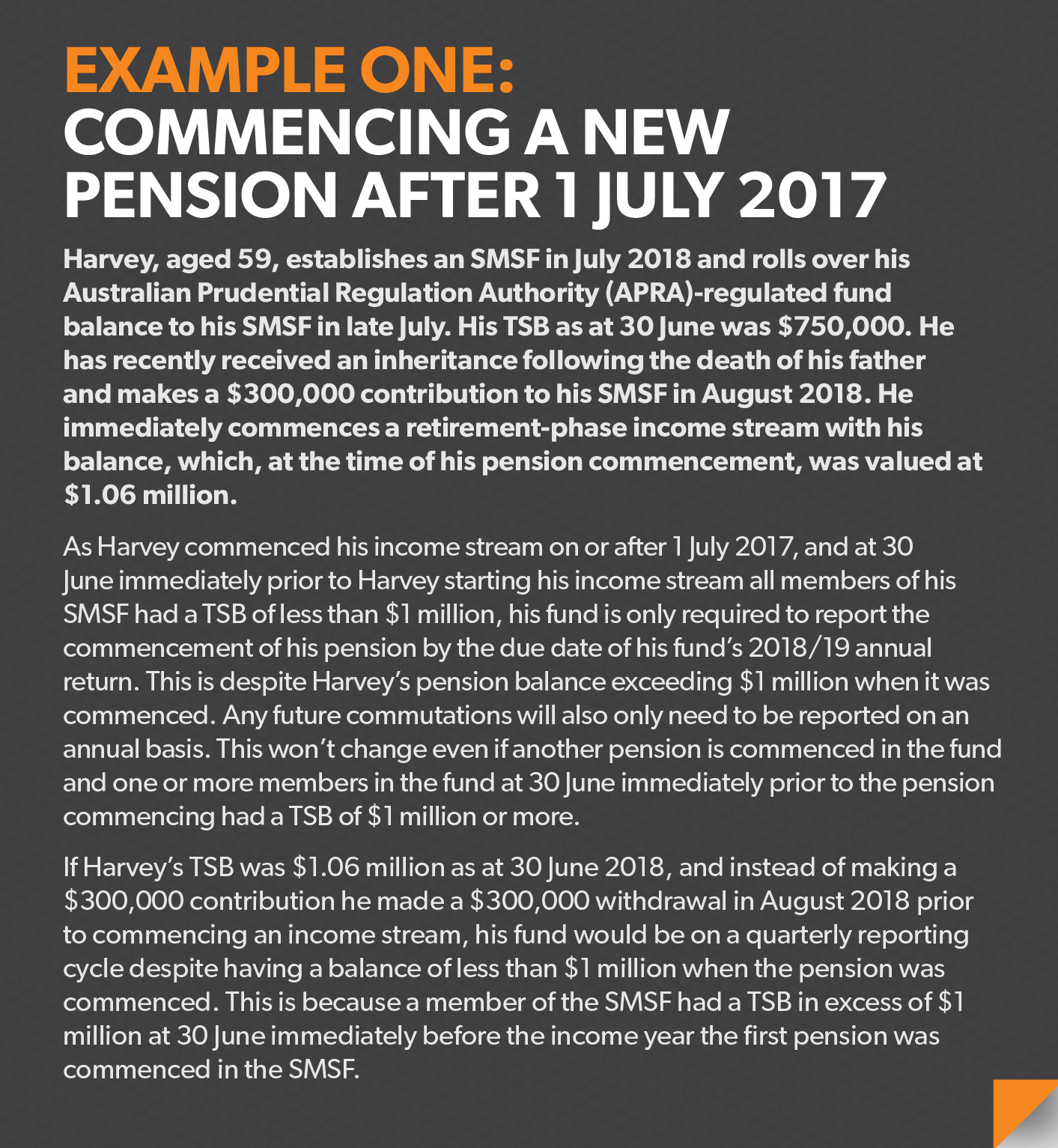

As example one illustrates, the requirement to use a member’s TSB at 30 June prior to assess the fund’s reporting frequency can give rise to situations where SMSFs will be required to report their TBA events on a quarterly reporting cycle even though the fund has no members with a TSB greater than $1 million when the first pension is commenced.

Similarly, there may be situations where an SMSF will only be required to report its TBA events on an annual basis despite the member’s TSB exceeding $1 million when the first pension is commenced in the fund.

SMSF advisers and trustees should be alert to these situations and, when applying the ATO’s relaxed reporting rule, should always determine the fund’s reporting frequency using member TSBs as at 30 June prior to the first pension being commenced, rather than at the date the first pension is commenced.

Given the member’s TSB at 30 June prior may not be known until well into the income year, care needs to be taken when commencing the first pension in the SMSF early in an income year as it may not always be possible to determine the fund’s actual TBA reporting frequency at that time.

Of course, there is a simple solution to the issues raised above and that is for the SMSF to report its TBA events on a more regular basis than that required by the ATO. More on this later.

Hidden dangers of deferred reporting

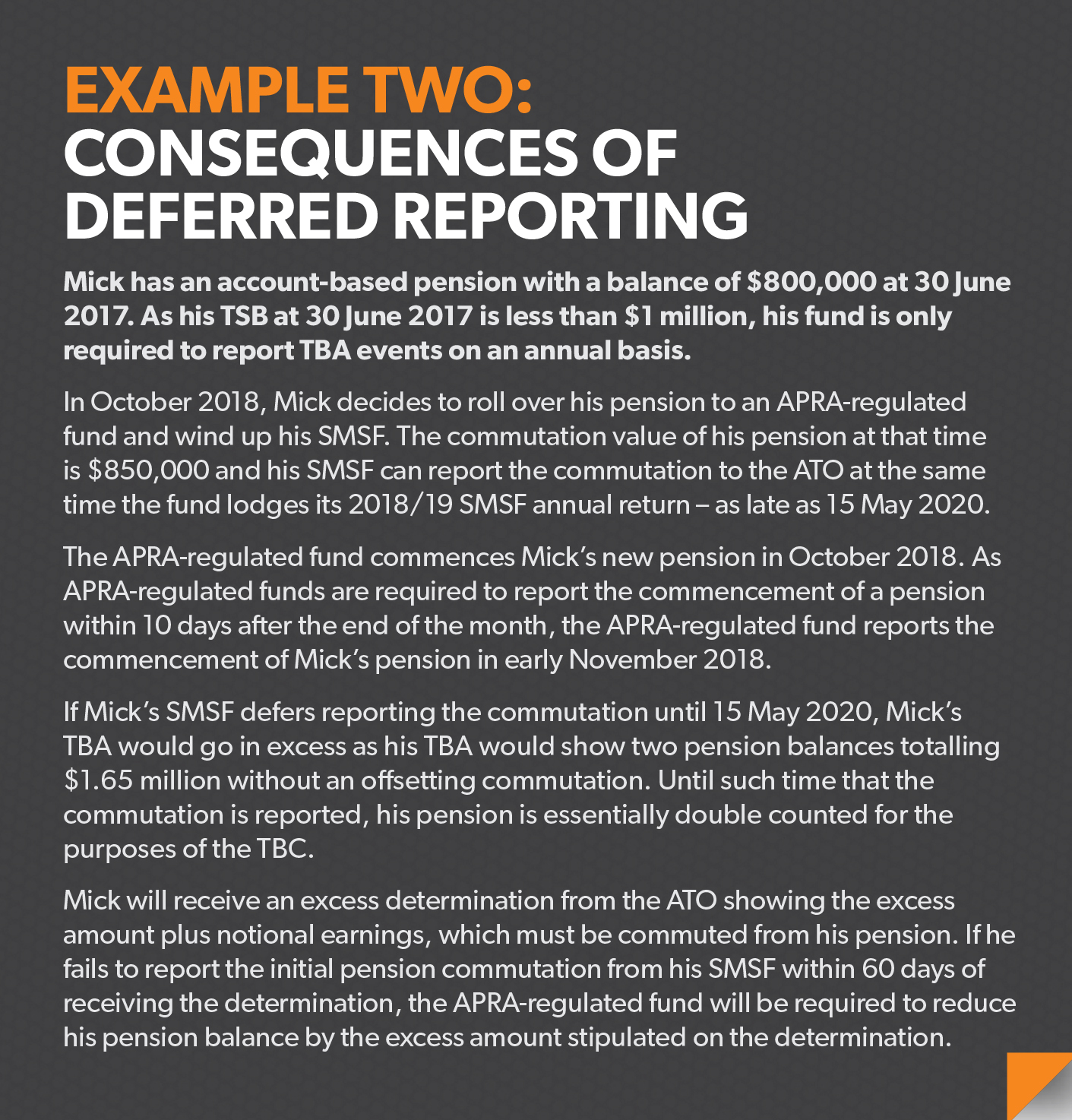

While the ATO has relaxed the event-based reporting rules for SMSFs, the tax penalties that could apply if a member exceeds their TBC have not been relaxed. SMSF members will incur excess transfer balance earnings for every day their pension balance exceeds their TBC, even though the event that gave rise to the excess may not be required to be reported to the ATO for 12 months or even longer.Admittedly, the $1 million threshold is designed to minimise situations where a member has an excess pension balance that goes undetected for extended periods of time, but mistakes can and will happen. This can lead to inadvertent TBC breaches and SMSF members having to pay more excess transfer balance tax than would have been the case if the event had been reported earlier and the excess amount removed sooner. SMSF members with capped defined benefit pensions in other funds are particularly vulnerable given they may be unfamiliar with the special value concept and the need to include this value when determining their overall TBC position.

It is worth noting that when reporting an event using the ATO’s transfer balance account report you are simply required to insert the ‘value’ of the pension. We have already seen instances where the account value of a market-linked pension has been reported incorrectly by clients as the value of the pension rather than the special value, being the annual entitlement multiplied by the remaining term.

Even where an excess pension balance is not the result of a reporting error or a member commencing a pension in excess of the cap, the deferred reporting of the relevant events may give rise to pension balances being commuted and possibly excess transfer balance tax being incurred.

The deferred reporting of TBA events can also have important estate planning implications. For example, if an SMSF member dies and their pension reverts to their spouse, it may be difficult for the reversionary spouse to calculate how much of the pension can revert, or how much of their pension needs to be commuted, if all events that have affected their TBC have not yet been reported to the ATO.

How can these risks be mitigated?

There is a simple solution to all of these issues and that is to ensure all events that impact on a member’s TBA are reported to the ATO on a monthly basis.

In other words, adopt the same reporting cycle that applies to APRA-regulated funds, which are generally required to report their TBA events 10 business days after the end of the month in which the event occurred. This would minimise the likelihood of incorrect determinations being issued by the ATO and would mean SMSF members and their advisers would be more able to rely on the ATO’s online information about their TBA. It would also avoid the possibility of penalties being imposed if the SMSF incorrectly assesses its reporting frequency.

Given the commutation value must be determined at the time the commutation is processed, the requirement to report pension commutations to the ATO on a monthly basis should not be an onerous imposition on the SMSF sector. While the intricacies of the TBC may lead to an increase in the number of pension commutations, there are systems and services available that can automate the reporting of these events to the ATO.

Admittedly, reporting the exact commencement value of a pension 10 business days after the end of the month in which the pension was started is not an easy task. SMSFs generally align the valuation of their assets with the completion of the fund’s end-of-year financial accounts. Therefore, it can be difficult and often not possible to determine the exact commencement value of the pension if these valuations and the fund’s tax position are not known at the time. But this is not an issue unique to the SMSF sector. APRA-regulated funds also face this same issue but find a way to determine the pension’s commencement value, presumably by adopting the reasonable estimate approach.

It is worth noting the ATO has stated it will accept a ‘reasonable estimate’ of the starting value of an income stream and the fund should record this value in its accounting records at the time of commencement. It is also worth noting a fund can report a revised starting value for the pension after the end-of-year accounts have been completed. However, care would need to be taken to ensure any adjustment to the pension’s starting value doesn’t result in the fund then failing to meet its minimum pension payment obligations.

It is difficult to see how the deferred reporting of events that impact on a member’s TBA is in the member’s best interest. This is particularly the case for pension commutations where it appears the member can only be disadvantaged by the deferred reporting of these events to the ATO.

Relying on the ATO’s relaxed reporting regime should be the exception to the rule rather than the standard reporting option. In many respects the ATO’s relaxed reporting rules should be regarded as a last resort reporting option and should only be relied on in situations where the risks of deferred reporting are known and have been fully assessed.